Transfer pricing

- Transfer pricing is the process of using a price to facilitate decentralized decision making by sharing information and aligning incentives within the firm.

Transfer pricing

- In simple examples like the initial questions in the Vik-Giger case it is easy to figure out what the price of a product should be.

Transfer pricing

- In that case we took for granted that we could easily quantify the costs of making the product.

- We also noted that transferring fixed costs (those that do not vary with output) is not at all simple.

Cost allocation

- Cost allocation is the process of connecting the sacrifice of resources (often a cash outflow) to the process, product, program, or department on behalf of which the resources were sacrificed.

Cost allocation

- We are trying to track who consumed which resources and when.

- We do this for many reasons and in many different contexts, so there is no one approach that is better in every situation.

Cost allocation

- Note that transfer pricing requires cost allocation, but not all cost allocations are done to support transfer pricing.

Which costs?

- We want to track all costs, but cost allocations focus on common, indirect, and overhead costs (all related terms)

- We allocate direct costs directly to the activities or products that consume them.

Cost allocation

- Most costs are direct at some point, and then flow into an area of the organization where they become indirect.

- For example, a networking department has many direct costs, but many departments access it indirectly.

Consider email

- we can easily track who uses it.

- we have good information about how much it costs.

- but it is difficult to define the relationship between email use and value creation in the design, manufacturing and sales department.

Consider aspirin administered in an American Hospital

- Aspirin costs $ 0.02 per tablet.

- How much is billed to the patient/insurer?

Consider aspirin administered in an American Hospital

| Direct Costs | Amount |

|---|---|

| Two aspirin tablets | $ 0.040 |

| Physician (Direct Labor) | $ 1.050 |

| Pharmacist (Direct Labor) | $ 1.330 |

| Nurse (Direct Labor) | $ 0.321 |

| Cup | $ 0.025 |

Continued

| Indirect Costs | Amount |

|---|---|

| Indirect labor (recordkeeping and orderly) | $ 0.800 |

| Shared and shifted costs: | |

| Unreimbursed Medicare | $ 0.450 |

| Indigent care | $ 0.332 |

| Malpractice insurance and uncollectible receivables | $ 0.380 |

| Excess bed capacity | $ 0.429 |

| Other administrative and operating costs | $ 0.688 |

| Product cost | $ 5.845 |

Continued

| Hopital Overhead Costs | Amount |

|---|---|

| Product cost | $ 5.845 |

| Hospital overhead costs @ 53.98\% | $ 3.16 |

| Full cost (incl. overhead) | $ 9.00 |

| Profit | $ 9.00 |

| Price (per dose) | $18.00 |

Is this an informative price?

Cost allocation is an old question

Indirect expense is one of the most important of all the accounts appearing on the books of the manufacturer. Methods of handling its [allocation] have given rise to more arguments than the descent of man. It is the rock upon which many a ship of industry has been wrecked.

- Thompson (1916)

Consider a manufacturing firm

May have many different allocation processes for a single product.

- Taxes (one set of depreciations, and FC allocations)

- Financial reporting

- Government contracts

- Other contracts

- Internal incentives

- Internal cost control

Reasons to allocate costs

- External reporting (IFRS, GAAP, also fraud)

- Taxes

- Cost-based contracts (esp. gov contracting)

- Decision making

- Incentives and accountability (‘control’)

Fraud is a financial accounting act, but a managerial accounting choice

- It is the act of misreporting which is illegal.

- However, without a performance incentive (explicit or implicit) misreporting is unlikely.

- Gambling for resurrection at FedEx.

- Investigation of the precursors of financial crimes at Goldman.

- Enron and Arthur Anderson (audit business was marketing for software business).

- Are you paying accountants for high-quality financial statements? Or for other forms of performance?

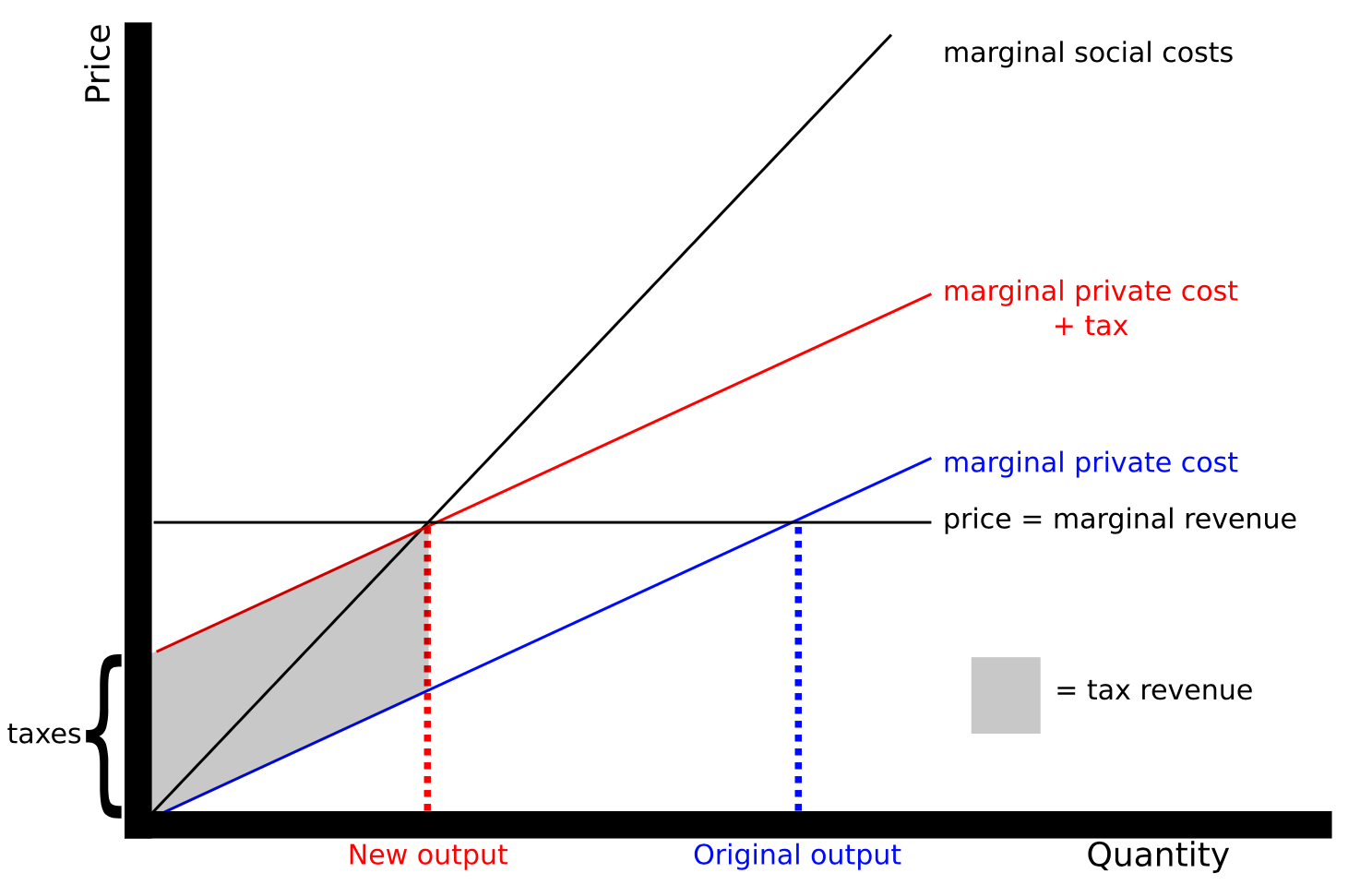

Incentive effects of cost allocations

- Cost allocations modify behavior a la Pigouvian taxes

- All cost allocations, like all taxes, modify behavior. They are never neutral.

Pigouvian tax

{ width=50% }

{ width=50% }

Why do we have common costs?

- The tax analogy helps us think about why cost allocations might be useful/harmful.

- But this reasoning doesn’t explain why we are ‘taxing’ aspirin in the hospital example.

- Common costs arise when it is less expensive to provide a good or service centrally.

Consider the following:

- A firm manufactures spinning hard drives and solid state hard drives

- The two divisions share a building but are separate profit centers

- Managers are compensated based on profits

How do we treat common costs?

- If we deduct common costs from the manager’s profits they will try to reduce common costs

- Use too little IT services.

- If we do not, then they will demand more of the common resources

- Use too much IT services.

- What we choose will depend on whether the managers can control their consumption of the common costs.

- Allocation of the factory itself?

- Allocation of cleaning crew?

- Allocation of IT?

- Allocating common costs is widespread, so overconsumption of common resources seems to be a common concern.

Make-up Exam Check

- One week from Tuesday, Canvas announcement as soon as the room is confirmed.