Cost Allocation in Practice

Allocating common costs

- Common costs: arise when it is less expensive to provide an internal product or service centrally.

- Consider: the two divisions of the hard drive manufacturer (SSD and HHD) share:

- building maintenance

- grounds

- property taxes security

- human resources department

Questions:

- Should the common costs be allocated to the manufacturing divisions?

- If so, how?

Considerations:

- division managers get paid for their division’s accounting profit

- cost allocations act like taxes and affect the managers’ welfare, and their behavior.

- if allocated, managers will seek to reduce costs by improving processes, cutting corners, or claiming not to need or use the common resource

- if not allocated, managers will seek to maximize use of the common resources

How should we interpret the status quo?

“Most firms allocate common costs, presumably to prevent individual divisions from overconsuming the common resource.” (Zimmerman Textbook)

- and yet, forcing firms to adopt cost accounting systems improves their performance, suggesting that some firms may just be using allocations from financial or tax accounting. (Samuels, 2021)

To allocate we need an allocation base/cost driver:

An allocation base or cost driver is the metric used to allocate costs (like the aspirin in the hospital example).

- Choosing an allocation base is one of the most important topics in all of accounting. Choosing correctly requires analysis of processes, data, and incentives.

- This focus on this critical aspect of accounting is missing from most texts and this course.

- In this lecture we will consider the consequences of these choices.

Insulating and non-insulating allocations

- the choice of driver can either insulate the manager’s pay from the cost or not.

A. Non-insulating method

A noninsulating method uses a driver that varies with the manager’s performance measures (e.g. div. operating income)

| Jan. HDD | Jan. SSD | Feb. HHD | Feb. SSD | |

|---|---|---|---|---|

| Div. Op. Income | $8,000 | $8,000 | $9,000 | $2,000 |

| Allocated costs | (800) | (800) | (900) | (200) |

| Net income | $7,200 | $7,200 | $8,100 | $1,800 |

This is a tax on operating income.

B. Insulating method

An insulating allocation uses a driver that does not vary with the manager’s performance measures (e.g. floorspace).

| Jan. HDD | Jan. SSD | Feb. HHD | Feb. SSD | |

|---|---|---|---|---|

| Div. Op. Income | $8,000 | $8,000 | $9,000 | $2,000 |

| Allocated costs | (600) | (400) | (600) | (400) |

| Net income | $7,400 | $7,600 | $8,400 | $1,600 |

This is a tax on floorspace.

Allocations in practice

- the allocation bases chosen (what to tax) affect the use of resources inside the firm.

- cost allocations also create incentives to cooperate.

- cost allocations can distort reported performance

Death spiral

- can occur when common costs consist primarily of fixed costs and users have discretion over their use of the common product or service.

Steps in the death spiral:

- The death spiral occurs when cost allocation reduces utilization of

a common resource (with significant fixed costs).

- i.e. the common cost is taxed, so it’s utilization falls.

- This creates excess capacity. Now the fixed cost is spread over fewer units of the allocation base.

- This increases the allocation rate for the remaining users (increasing the ‘tax’ rate), which further reduces utilization.

Death Spiral (not literal) in Corporate Jets

- The annual operating cost of a corporate jet ranges between $40 and $50 million.

- Corporate flight departments routinely charge part or all of these costs to those internal departments using the aircraft.

- Allocating operating costs to internal users allows flight departments to justify the expense of the aircraft to top management, to apportion operating costs according to usage patterns, and to prevent overscheduling.

Death Spiral (not literal) in Corporate Jets

- Initially, only the direct operating costs (fuel and landing fees) were charged back to departments using the aircraft, while fixed costs were not (pilot salaries, maintenance costs, hangar rental, and insurance).

These costs are all variable, so no (figurative) danger

Death Spiral (not literal) in Corporate Jets

- When firms faced downturns in their business, a popular expense reduction target was to cut corporate jet usage by allocating the fixed costs along with the direct costs of operating the aircraft.

This makes sense, but now we are allocating fixed costs, and managers can choose how much to use! But their choice does not change the fixed costs.

Death Spiral (not literal) in Corporate Jets

- Since fixed costs accounted for about 50 percent of the total cost at full utilization, usage rapidly shrank to the point where fixed costs rose to 85 percent of the total allocated cost.

What happens when taxes go up?

Death Spiral (not literal) in Corporate Jets

- Jet usage dropped further, and each flight hour allocated became even more costly, sometimes approaching the cost of chartering a jet.

- At this point there is no economy of scale and no reason to produce the service internally!

Can we avoid this?

- When there is excess capacity only allocate the variable cost of the resource.

- Alternatively, some of the fixed costs could be excluded from the transfer price.

- Using practical capacity instead of actual utilization in calculating the overhead rate.

A caution:

If you are not careful, you might use arithmetic to convince yourself that adding new products or services may decrease fixed costs.

No production decision, other than actually changing the fixed costs themselves, can change fixed costs.

Allocating capacity cost: depreciation

- Not allocating some (or all) of the fixed cost can reduce the death spiral.

- For example, allocate only the fixed cost of the capacity actually being used.

- If 40 percent excess capacity exists, allocate only 60 percent of the depreciation.

- However, this solution to the death spiral creates other concerns.

Allocating capacity cost: depreciation

- How much of the existing common resource should each user use?

- The current capacity level was chosen for some reason!

- If excess capacity exists, any charge discourages its use.

- Allocating accounting depreciation to users commits them to recovering at least the historical cost of the asset.

The trade-off

When allocating depreciation the firm trades off:

- the efficient investment in the common resource and

- its efficient utilization after acquisition.

On one hand… on the other hand:

Charging depreciation helps control the overinvestment problem, but at the expense of underutilizing the asset after acquisition.

Most firms charge users for depreciation.

Control of overinvestment is the habit of financial accounting systems

- Control of the overinvestment problem tends to dominate decision-making errors involving asset utilization (the death spiral).

- This is another example of how accounting systems tend to favor control when confronted with a choice between control and decision making.

- This doesn’t mean that it is the optimal decision.

Getting this right matters!

Cost Allocations at IBM:

During the 1980s and early 1990s, IBM had the policy of allocating costs from one line of business to another. Managers in those lines of business constantly argued that some of their overhead should be carried by other IBM businesses.

Cost Allocations at IBM:

IBM also typically allocated all of the R&D of a new technology to the line of business first using the technology, and subsequent users were able to utilize it for free.

Cost Allocations at IBM:

This cost allocation system masked the true profitability of many IBM businesses for years. IBM claimed it was making money in its PC business.

Cost Allocations at IBM:

But in 1992, “as IBM began to move away from its funny allocation system, IBM disclosed that its PC business was unprofitable.” In 2004, IBM sold its PC division to China-based Lenovo Group for $1.75 billion.

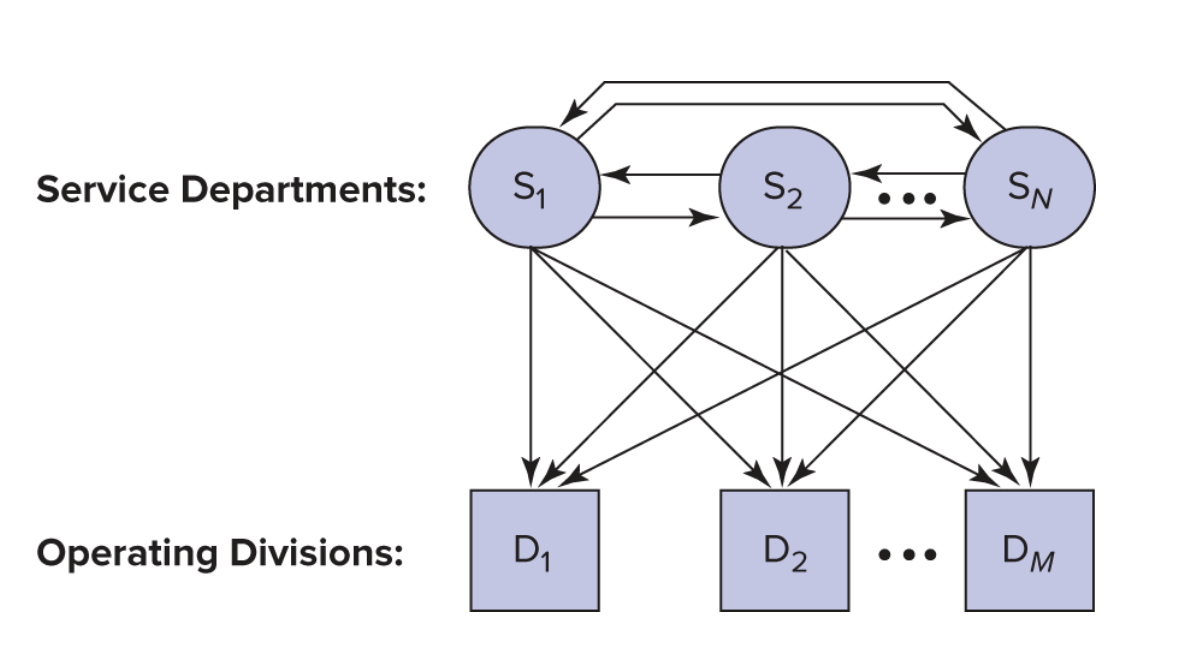

Allocating service department costs

Now that we’re clear on all the things that can go wrong, lets try to do it!

Allocating service department costs

Example:

Capacity of service departments used:

| Telecoms | IT | Cars | Trucks | Total | |

|---|---|---|---|---|---|

| Telecoms | 10% | 20% | 40% | 30% | 100% |

| IT | 25% | 15% | 35% | 25% | 100% |

Service department costs:

| Cost | |

|---|---|

| Telecoms | 2,000,000 |

| IT | 6,000,000 |

| Total | 8,000,000 |

Direct method

Service dept actual usage allocation:

| Cars | Trucks | Tot Alloc | Tot Incur | Tot Unalc | |

|---|---|---|---|---|---|

| Telecoms | $0.8 | $0.6 | $1.4 | $2.0 | $0.6 |

| (40% × $2) | (30% × $2) | ||||

| IT | $2.1 | $1.5 | $3.6 | $6.0 | $2.4 |

| (35% × $6) | (25% × $6) | ||||

| Total | $5.0 | $8.0 | $3.0 |

(Dollars are in millions)

Direct allocation method:

| Shares | Cars | Trucks | Total |

|---|---|---|---|

| Telecoms | 40%/(40% + 30%) = 4/7 | 30%/(40% + 30%) = 3/7 | 100% |

| IT | 35%/(35% + 25%) = 7/12 | 25%/(35% + 25%) = 5/12 | 100% |

| Allocated Costs | Cars | Trucks | Total |

|---|---|---|---|

| Telecoms | 4/7 × $2 = $1.143 | 3/7 × $2 = $0.857 | $2 |

| IT | 7/12 × $6 = $3.500 | 5/12 × $6 = $2.500 | $6 |

| Total | $4.643 | $3.357 | $8 |

Good news, Bad news

- Good news: everything is allocated

- Bad news: this is not a good estimate of opportunity cost per unit of service

What we know:

While we do not know the correct opportunity cost, we do know that the direct allocation method excludes the service departments’ use of other service departments and therefore incorrectly states the opportunity cost of each service department.

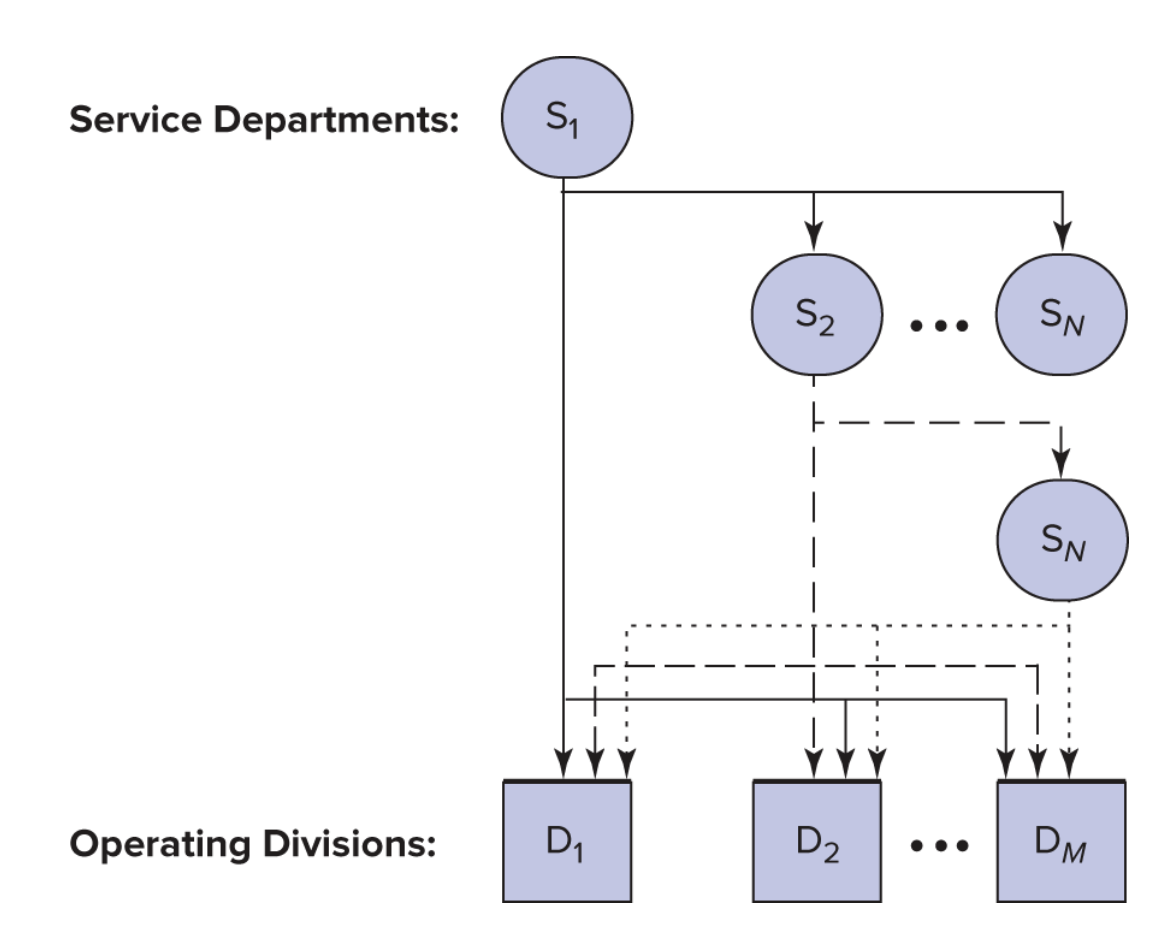

Step-down method

Step-down shares (start w/ Tele)

| IT | Cars | Trucks | Total | |

|---|---|---|---|---|

| Telecoms | 20%/(20% + 40% + 30%) | 40%/90% | 30%/90% | |

| = 2/9 | = 4/9 | = 1/3 | 100% | |

| IT | None | 35%/60% | 25%/60% | |

| = 7/12 | = 5/12 | 100% |

Step-down allocations

| Costs to Allocate | IT | Cars | Trucks | Total Alloc. | |

|---|---|---|---|---|---|

| Telecoms | $2 | 2/9 × $2 | 4/9 × $2 | 1/3 × $2 | |

| = $0.444 | = $0.889 | = $0.667 | $1.556 | ||

| IT | $6 + $0.444 | None | 7/12 × $6.444 | 5/12 × $6.444 | |

| = $3.759 | = $2.685 | $6.444 | |||

| Total | $4.648 | $3.352 | $8.000 |

Does the order matter?

It may! In this case the difference in magnitudes is relatively minor.

Step-down shares (start w/ IT)

| Telecoms | Cars | Trucks | Total | |

|---|---|---|---|---|

| IT | 25%+/(25% + 35% + 25%) | 35%/85% | 25%/85% | 100% |

| = 5/17 | = 7/17 | = 5/17 | 100% | |

| Telecoms | None | 4/7 | 3/7 | 100% |

Step-down allocations

| Costs to Allocate | IT | Cars | Trucks | Total Alloc. | |

|---|---|---|---|---|---|

| IT | $6 | 5/17 × $6 | 7/17 × $6 | 5/17 × $6 | |

| = $1.765 | = $2.470 | = $ 1.765 | $4.235 | ||

| Telecoms | $2 + $1.765 | None | 4/7 × $3.765 | 317 × $3.765 | |

| = $ 2.151 | = $ 1.614 | $3.765 | |||

| Total | $4.6210 | $3.379 | $8.000 |

costs are in millions.

Does the order matter?

Does the order matter?

- The costs allocated to Cars and Trucks differ by only $27,000

depending on whether telecommunications or IT is chosen first.

- The difference of $27,000 is less than 1 percent of the total costs allocated.

Does the order matter?

- However, very different incentives result depending on which method is used.

- Allocated costs are taxes, and taxes effect behavior.

- And these can lead to the Death Spiral if the tax is too high!

Illustration:

- To illustrate lets expand the telecommunications and IT example.

- Suppose the allocation base in telecommunications is the number of telephones in each department, and

- in IT the allocation base is the number of gigabytes of disk space used.

Illustration:

- Transfer prices are to be established for telephones and gigabytes.

- Allocated costs will be used to compute the transfer prices.

The allocation bases:

| Allocation base | |

|---|---|

| Telecomm | 3,000 Telephones |

| IT | 12 million gigabytes |

Cost allocated per phone

Number of phones

| Direct | Step, Telecomm first | Step, IT first | |

|---|---|---|---|

| Telecoms | – | – | – |

| IT | – | 20% × 3.000 = 600 | – |

| Cars | 40% × 3,000 = 1,200 | 40% × 3,000 = 1,200 | 40% × 3,000 = 1,200 |

| Trucks | 30% × 3,000 = 900 | 30% × 3,000 = 900 | 30% × 3,000 = 900 |

| Phones | 2,100 | 2,700 | 2,100 |

- Note: that telecom is always ‘–’ here because we are considering how to allocate it’s costs. The in the ‘IT first’ column the telecom costs already include IT costs.

Cost allocated per phone

| Direct | Step, Telecomm first | Step, IT first | |

|---|---|---|---|

| Cost per phone | $2M/2.100 | $2M/2.700 | $3.765M/2.100 |

| = $ 952 | = $ 741 | = $1.793 | |

| Number of phones: Cars | 1,200 | 1,200 | 1,200 |

| Telecoms charged to Cars | $1.143 | $0.889 | $ 2.151 |

Does the order matter?

The order can lead to large changes in the ‘tax’ on the allocation base!

Cost allocated per Gigabyte of Storage

Number of Gigabytes of Storage

| Direct | Step, Telecomm first | Step, IT first | |

|---|---|---|---|

| Telecoms | – | – | 25% × 12 = 3.0 |

| IT | – | – | – |

| Cars | 35% × 12 = 4.2 | 35% × 12 = 4.2 | 35% × 12 = 4.2 |

| Trucks | 25% × 12 = 3.0 | 25% × 12 = 3.0 | 25% × 12 = 3.0 |

| Gigs | 7.2 | 7.2 | 10.2 |

- Note: that IT is always ‘–’ here because we are considering how to allocate it’s costs. The in the ‘Telecom first’ column the IT costs already include Telecom costs.

Cost allocated per Gigabyte of Storage

| Direct | Step, Telecomm first | Step, IT first | |

|---|---|---|---|

| Cost per gig | $6/7.2 = $0.833 | $6.44/7.2 = $0.895 | $6/10.2 = $0.588 |

| Number of gigs in Cars | 4.2 | 4.2 | 4.2 |

| IT charged to Cars | $3.5 | $3.759 | $2.470 |

Cost allocated per Giga of storage (Millions except cost per Gb)

Consider the impact on behavior:

- The sequence of service departments in the step-down method changes the costs of each service.

- Because the cost per phone (which represents the transfer price) varies depending whether or not it includes IT costs,

- the cost allocation scheme affects the decision of each department to add or drop phones.

- The same conclusions hold for the information technology department.

Does the order matter?

- Note the wide variation in cost per gigabyte.

- The cost varies from $0.588 per gigabyte under the step-down method with IT chosen first

- to $0.895 under the step-down method with telecommunications chosen first.

The central issues with the step-down method:

- The sequence used is arbitrary and large differences can result in the cost per unit of service using different sequences.

- Also, the step-down method ignores the fact that although departments earlier in the sequence use service departments later in the sequence, earlier departments are not allocated these costs.

- Get this wrong and risk the death spiral.

Step-Down Allocations and Medicare

Step-Down Allocations and Medicare

- The U.S. Medicare system requires each hospital to file a Medicare Cost Report to get reimbursed for providing health care to Medicare patients.

- To file this report, all cost centers in the hospital (administration, finance, human resources) that supply services to other cost centers and major functional services, such as the emergency department, surgery, and maternity, are ordered in a step-down sequence.

Step-Down Allocations and Medicare

- Each cost center allocates its cost using an allocation base.

- For example, nursing administration costs might be allocated using nursing hours or nursing salaries in each functional service.

Step-Down Allocations and Medicare

- The Medicare Cost Report defines the order of the cost centers to be used in the step-down method but allows each hospital some discretion.

- For example, administration and general costs are usually allocated last. -However, some hospitals move it up in the list.

Step-Down Allocations and Medicare

- The step-down method allocates the cost of each service center, as well as the costs stepped down to it, to the major functional services.

- Many hospitals use the data generated by the Medicare Cost Report to set prices and to negotiate third-party contracts.

- Note that the Medicare system is one of the few parts of the US health system that actually works!

SOURCE: M. Muse and B. Amoia, “Step Up to the Step-Down Method,” Healthcare Financial Management, May 2006.

Next class

We will try to improve on the step-down method.